Data Center Interconnect Market Overview

The Data Center Interconnect (DCI) market is witnessing significant growth due to the increasing demand for cloud services, digital transformation, and the rapid expansion of data centers worldwide. DCI technologies are designed to connect two or more data centers over short, medium, or long distances, enabling high-speed data transfer, backup, disaster recovery, and business continuity. The adoption of virtualization and cloud-based solutions is driving the need for robust DCI solutions that can support high bandwidth, low latency, and secure connectivity.

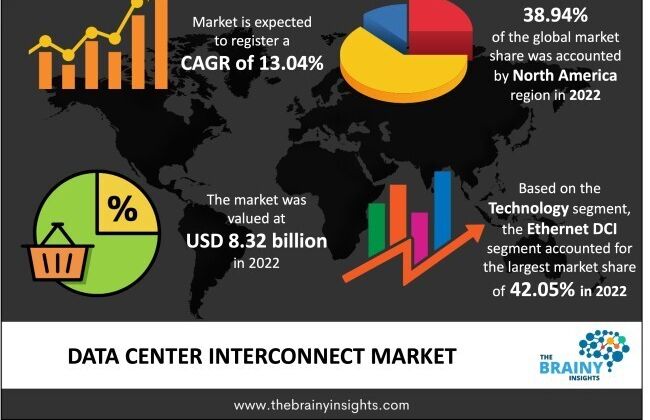

Valued at USD 8.32 billion in 2022, the global data center interconnect (DCI) market is projected to grow at a compound annual growth rate (CAGR) of 13.04% from 2023 to 2032, reaching an estimated USD 28.34 billion by the end of the forecast period.

Market Dynamics

Drivers:

• Rising Cloud Adoption: The exponential growth in cloud computing and SaaS platforms is a key driver.

• Big Data and IoT: The explosion in data generated by IoT devices and analytics platforms necessitates efficient data transfer across locations.

• Business Continuity & Disaster Recovery Needs: Organizations require resilient infrastructure to ensure seamless operations.

• Growing Demand for High Bandwidth Applications: Video streaming, AI/ML applications, and real-time data processing fuel demand.

Restraints:

• High Initial Investment: Implementation of DCI solutions involves significant capital expenditure.

• Complexity in Integration: Integrating DCI with legacy systems can be challenging.

Opportunities:

• Emerging Markets and Edge Data Centers: Expanding infrastructure in APAC, Latin America, and edge computing are major growth areas.

• 5G Deployment: Increased data movement and low latency demands from 5G services.

Regional Analysis

• North America: Leading the market due to a high concentration of cloud service providers, hyperscale data centers, and advanced IT infrastructure.

• Europe: Rapid adoption of cloud technologies, strong regulatory frameworks around data privacy (GDPR), and green data center initiatives.

• Asia-Pacific: Fastest growing region, driven by digitalization efforts, increasing internet penetration, and expanding colocation services in countries like China, India, and Singapore.

• Middle East & Africa: Gradual adoption of data center technologies with increased investment in IT infrastructure.

• Latin America: Emerging market with growing demand for colocation and managed services.

Segmental Analysis

By Type:

• Cloud-based DCI

• Inter-data Center (IDC) DCI

• Campus DCI

By Component:

• Solutions (Hardware & Software)

• Services (Managed & Professional)

By Application:

• Disaster Recovery & Business Continuity

• Data Backup & Storage

• Real-time Data Replication

By Industry Vertical:

• IT & Telecom

• BFSI

• Healthcare

• Media & Entertainment

• Government

List of Key Players

• Cisco Systems, Inc.

• Huawei Technologies Co., Ltd.

• Ciena Corporation

• Nokia Corporation

• Juniper Networks, Inc.

• Infinera Corporation

• Equinix, Inc.

• ADVA Optical Networking

• ZTE Corporation

• Fujitsu Ltd.

Key Trends

• Adoption of SDN and NFV in DCI to enable dynamic and scalable interconnections.

• Edge Computing Integration to improve latency and bandwidth efficiency.

• Automation and AI in Network Management for predictive maintenance and optimization.

• Expansion of Hyperscale Data Centers to support global cloud networks.

• Green Data Centers & Energy Efficiency becoming a strategic focus.

Request PDF Brochure: https://www.thebrainyinsights.com/enquiry/sample-request/12568

Conclusion

The Data Center Interconnect market is poised for robust growth fueled by the digital revolution, cloud migration, and the continuous need for high-performance networking. Innovations in optical networking, automation, and software-defined infrastructures will shape the future of DCI, ensuring secure, scalable, and resilient data center communication across the globe.

Top comments (0)