Zero Trust Security Market Overview

Market Overview

The Zero Trust Security market is experiencing rapid growth driven by increasing cyber threats, the adoption of cloud technologies, and a shift toward a perimeter-less security model. Zero Trust architecture, based on the principle of “never trust, always verify,” ensures that only authenticated and authorized users and devices can access applications and data.

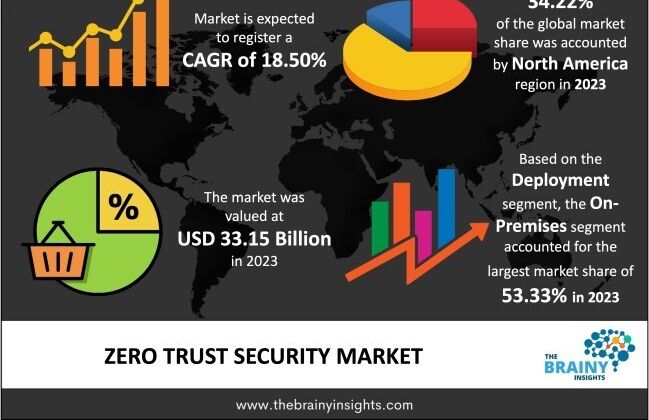

The zero trust security market is projected to reach USD 181.02 billion by 2033, growing at a CAGR of 18.50% between 2024 and 2033.

Market Dynamics

Drivers

• Rising Cybersecurity Threats: An increasing number of sophisticated cyberattacks, including ransomware and insider threats, is pushing organizations to adopt Zero Trust frameworks.

• Cloud Adoption: Migration to cloud infrastructure demands more robust and granular access controls, enhancing Zero Trust adoption.

• Regulatory Compliance: Regulations such as GDPR, HIPAA, and CCPA are encouraging companies to secure sensitive data more strictly.

Restraints

• Complex Implementation: Integrating Zero Trust with existing systems can be complex and resource-intensive.

• High Initial Costs: Despite long-term savings, the upfront investment in tools and training can deter some organizations.

Opportunities

• SMEs Adopting Cloud & SaaS: Smaller businesses moving to digital platforms are increasingly seeking scalable Zero Trust solutions.

• Integration with AI & ML: Advanced analytics and behavioral monitoring are enhancing threat detection and real-time responses.

Regional Analysis

• North America: Dominates the market due to early technology adoption, strong cybersecurity infrastructure, and presence of key players.

• Europe: Strong growth driven by GDPR compliance and increasing investment in cybersecurity.

• Asia-Pacific: Fastest-growing region, led by increasing digital transformation, especially in India, China, and Southeast Asia.

• Latin America & MEA: Gradual adoption, with growing awareness and investments in banking, government, and critical infrastructure sectors.

Segmental Analysis

By Component

• Solutions: Identity and Access Management (IAM), Security Analytics, Data Security, Microsegmentation, Network Security.

• Services: Integration & Implementation, Support & Maintenance, Consulting.

By Deployment Mode

• Cloud-Based

• On-Premises

By Organization Size

• Large Enterprises

• Small and Medium Enterprises (SMEs)

By Industry Vertical

• BFSI

• Healthcare

• IT & Telecom

• Government

• Retail

• Energy & Utilities

Key Players

• Microsoft Corporation

• IBM Corporation

• Cisco Systems, Inc.

• Palo Alto Networks

• Okta, Inc.

• Akamai Technologies

• Google LLC (BeyondCorp)

• Zscaler, Inc.

• Fortinet, Inc.

• VMware, Inc.

These companies are focusing on partnerships, acquisitions, and product innovations to expand their Zero Trust portfolios.

Key Trends

• Rise of Secure Access Service Edge (SASE)

• Integration of AI/ML in Zero Trust

• Focus on Identity-Centric Security

• Growing Adoption in Remote Work Environments

• Use of Behavioral Biometrics for Authentication

Request PDF Brochure: https://www.thebrainyinsights.com/enquiry/sample-request/12860

Conclusion

The Zero Trust Security market is at a critical growth juncture as organizations worldwide strive to secure complex and distributed IT environments. As digital transformation accelerates and threats evolve, Zero Trust is becoming the cornerstone of modern cybersecurity strategies.

Top comments (0)